Electronic Fund Transfer Act (EFTA) Policy and Procedures

Last modified: March 8th, 2026.

POLICY STATEMENT

It is the policy of Shift Connect Global dba Pay From Away (“Pay From Away”) to comply with the requirements of the Electronic Fund Transfer Act (15 U.S.C. 1693) (“EFTA”) and Regulation E (12 C.F.R. Part 1005), as applicable. Pay From Away permits consumers to initiate, authorize, and review electronic fund transfer (“EFT”) activity in connection with services offered through Pay From Away’s website at https://www.payfromaway.io.

This policy directs management to implement and maintain protocols defining the rights, liabilities, and responsibilities of each participant in the EFT system. The Pay From Away management team is responsible for staying informed about the laws and regulations governing these transactions and ensuring that Pay From Away consistently adheres to applicable legal and regulatory requirements.

COVERAGE

This policy covers EFTs and related remittance transfer activities, as applicable, where Pay From Away facilitates, processes, receives, holds, disburses, debits, or credits funds in connection with consumer payments made through its services.

KEY DEFINITIONS

Access device means a card, code, password, login credential, or other means of access to a consumer’s account or payment profile, or any combination thereof, that may be used by the consumer to initiate EFTs or access transaction information.

Account means a consumer asset account established primarily for personal, family, or household purposes and accessed in connection with Pay From Away’s services, including, where applicable, an account through which a consumer initiates or authorizes an EFT or accesses transaction information through Pay From Away’s website.

For purposes of this policy, references to “consumer” or “accountholder” mean a natural person.

Electronic fund transfer (EFT) means any transfer of funds initiated through an electronic terminal, telephone, computer, or magnetic tape for the purpose of ordering, instructing, or authorizing a financial institution or payment provider to debit or credit a consumer’s account.

The term includes, but is not limited to:

- Point-of-sale transfers;

- Automated teller machine (ATM) transfers;

- Direct deposits or withdrawals of funds;

- Transfers by telephone;

- Transfers resulting from debit card transactions, whether or not initiated through an electronic terminal;

- Payroll and gift cards; and

- Electronic check conversions (ECKs).

The term electronic fund transfer (EFT) does not include:

- Checks or drafts;

- Check guarantee or authorization programs;

- Wire or other similar transfers;

- Securities and commodities transfers; and

- Automatic transfers by the account-holding institution.

The term error means:

- An unauthorized EFT;

- An incorrect EFT to or from the consumer’s account;

- The omission of an EFT from a periodic statement or transaction history;

- A computational or bookkeeping error made by Pay From Away relating to an EFT;

- The consumer’s receipt of an incorrect amount of money from an electronic terminal;

- An EFT not identified correctly; or

- The consumer’s request for documentation or for additional information or clarification concerning an EFT, including a request made by the consumer to determine whether an error exists.

The term error does not include:

- A routine inquiry about the consumer’s account balance or payment status;

- A request for information for tax or other recordkeeping purposes; or

- A request for duplicate copies of documentation.

Preauthorized electronic fund transfer means an EFT authorized in advance to recur at substantially regular intervals.

References in this policy to online access, transaction information, disclosures, statements, or account information mean access provided through Pay From Away’s website at https://www.payfromaway.io.

DISCLOSURE REQUIREMENTS

Disclosures required under Regulation E must be clear, readily understandable, in writing, and in a form the consumer may keep.

Transactional Disclosures

For transactions involving an EFT service, the consumer will receive transaction confirmations, or in some cases pro forma confirmations, that include applicable disclosures.

The contents of such disclosures will include, as applicable:

- A summary of the consumer’s liability for unauthorized EFTs as set forth under Regulation E and under applicable law or agreement;

- The telephone number, email address, mailing address, and website contact information the consumer should use if they discover an error or require assistance;

- Pay From Away’s business days;

- The types of EFTs the consumer may make and any limitations on the frequency and dollar amount of transfers;

- Any fees Pay From Away imposes for EFTs or for the right to make transfers;

- A summary of the consumer’s right to receipts and periodic statements, transaction histories, or similar records made available through Pay From Away’s website;

- A summary of the consumer’s right to stop payment of a preauthorized EFT and the procedure for placing a stop-payment order;

- A summary of Pay From Away’s liability to the consumer for failure to make or stop certain transfers;

- The circumstances under which, in the ordinary course of business, Pay From Away may provide information concerning the consumer’s account or transactions to third parties; and

- A notice substantially similar to the model form in the regulation concerning error resolution.

For purposes of this policy, Pay From Away’s contact information is:

Pay From Away

Website:

https://www.payfromaway.io/

Email:

support@payfromaway.io

Phone:

877-577-4438

Mailing Address:

323 10 Ave SW #310, Calgary, AB T2R 0A5

Business Days:

Monday to Friday, 7:00 a.m. to 5:00 p.m. MST

STATEMENTS

Pay From Away will provide consumers with access to applicable transaction and account information relating to EFT activity through Pay From Away’s website at https://www.payfromaway.io. Consumers who have login credentials may access available account information, transaction details, and related records through the website. If a consumer requires copies by email, Pay From Away may generate and provide such copies upon request.

Statements, summaries, or transaction records, which may include information regarding transactions other than EFTs, will disclose, as applicable:

- The amount involved and the date the transfer is initiated;

- The type of transfer;

- The identity of the consumer or payment profile associated with the transaction;

- The identity of any third party to whom or from whom funds are transferred, where applicable;

- The amount of any fee or charge assessed by Pay From Away during the covered period for EFTs;

- Available balance or transaction history information, where applicable; and

- The contact information to be used to ask about a statement or report an error.

ERROR RESOLUTION DISCLOSURE AND PROCEDURES

As part of the initial disclosure, the consumer will be informed of the measures to be taken to resolve errors relating to the account or transaction record as a result of:

- An unauthorized transfer made by someone who has no authority to transfer funds from the account;

- A transfer that is omitted when the electronic system malfunctions;

- A computer or bookkeeping error;

- A failure to identify an EFT on a receipt, notice, or statement required by the regulation; and

- A consumer request for additional information or clarification concerning an EFT.

Pay From Away will also provide a short-form error resolution notice with each transaction confirmation disclosure, where required.

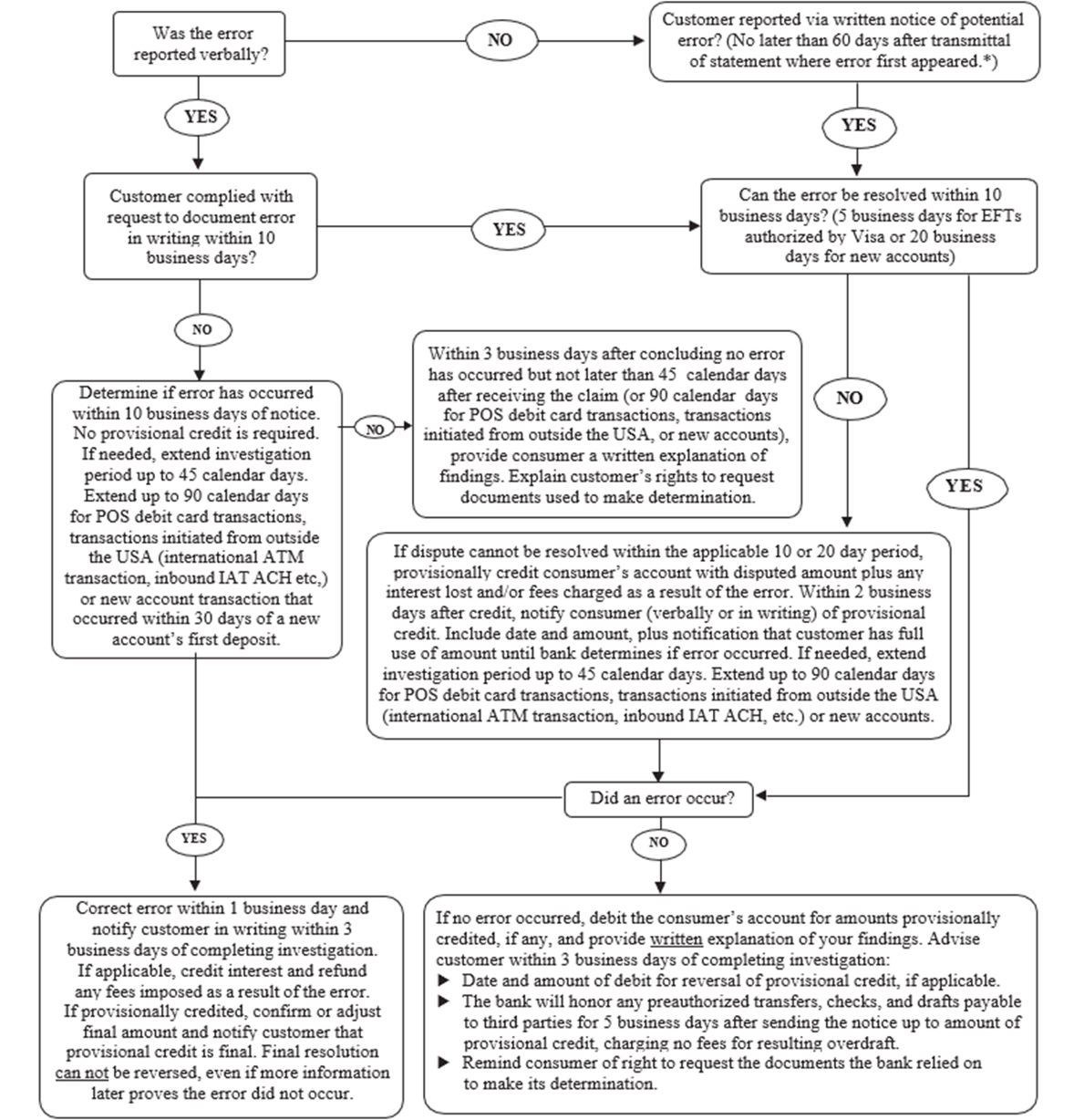

In general, if Pay From Away receives a written notice of error from a consumer, Pay From Away will investigate and determine whether an error occurred within 10 business days of receiving the notice of error. Pay From Away will report the results to the consumer within three business days after completing the investigation and will correct the error within one business day after determining that an error occurred.

If Pay From Away is unable to complete its investigation within 10 business days, or within 20 business days if the notice of error involves an EFT to or from an account within 30 days after the first deposit was made to the account, Pay From Away may take up to 45 days from receipt of the notice of error to investigate and determine whether an error occurred. However, in order to extend the investigation period, Pay From Away must provisionally credit the consumer’s account in the amount of the alleged error, including interest where applicable, and allow the consumer full use of the funds during the investigation.

Pay From Away may take up to 90 days to investigate an error involving an EFT that:

- Was not initiated within a state.

Consumers should notify Pay From Away as soon as possible by using the contact information available on https://www.payfromaway.io, by emailing support@payfromaway.io, by calling 877-577-4438, or by mail at 323 10 Ave SW #310, Calgary, AB T2R 0A5.

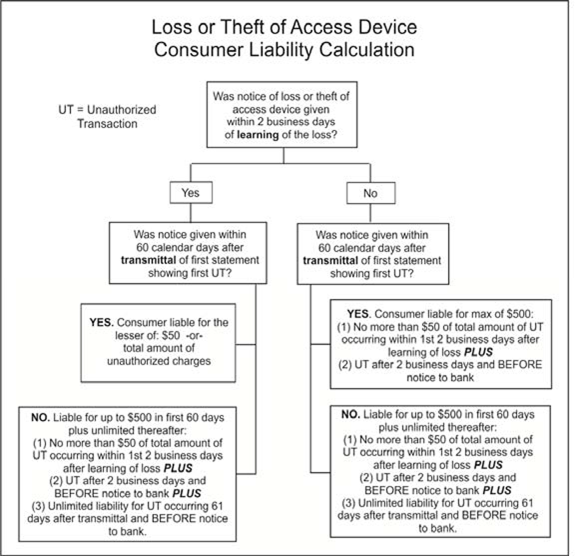

ACCOUNTHOLDER LIABILITY FOR UNAUTHORIZED TRANSACTIONS

Pay From Away may hold a consumer liable for an unauthorized EFT involving the consumer’s account, provided that accurate disclosures have been given and the consumer has not provided timely notice.

A consumer must report an unauthorized EFT that appears on a periodic statement or transaction record within 60 days of Pay From Away’s transmittal or provision of the statement or record in order to avoid liability for subsequent transfers. If the consumer fails to do so, and Pay From Away establishes that the unauthorized EFT would not have occurred had the consumer notified Pay From Away within the 60-day period, the consumer’s liability will not exceed the amount of the unauthorized transfers that occur after the close of the 60 days and before notice to Pay From Away.

If timely notice is given, the consumer’s liability will not exceed the lesser of $50 or the amount of unauthorized transfers that occur before notice to Pay From Away.

If state law or an agreement between the consumer and Pay From Away imposes less liability than is provided by this section, the consumer’s liability will not exceed the amount imposed under the applicable state law or agreement.

REMITTANCE TRANSFERS

For remittance transfers, Pay From Away will comply with Subpart B of Regulation E.

In general, the term remittance transfer is used to describe consumer transfers of funds sent by a remittance transfer provider, whether or not the sender is an accountholder and regardless of whether the transaction is also an EFT.

Consumers may transfer funds to recipients in foreign countries by wire transfer or automated clearinghouse (ACH) transactions. Consumers in the United States may also transfer funds to businesses as well as individuals in foreign countries, for example to pay bills, tuition, or other expenses. The Dodd-Frank Act defines “remittance transfer” broadly to include most electronic transfers of funds sent by consumers in the United States to recipients in other countries.

In the United States, remittance transfers sent by financial institutions or providers are generally subject to federal anti-money laundering laws and restrictions on transfers to or from certain persons. Consumer protections for remittance and other funds transfers may vary at the state level, and international money transfers may fall outside the scope of some other federal consumer protection frameworks.

Coverage

A remittance transfer generally includes a transfer that is:

- More than $15;

- Made by a consumer in the United States; and

- Sent to a person or company in a foreign country.

Examples of remittance transfers include:

- Transfers where the sender provides payment and requests Pay From Away to send the funds to a specified location or account in a foreign country;

- Consumer wire transfers where Pay From Away executes a payment order at the sender’s request to wire money from the sender’s account to a designated recipient;

- International ACH transactions sent from the sender’s account at the sender’s request; and

- Online bill payments and other electronic transfers that a sender schedules in advance, including preauthorized remittance transfers, made at the sender’s request to a designated recipient.

Transfers that are not covered include:

- A consumer’s use of a debit, credit, or prepaid card directly with a foreign merchant as payment for goods or services, because the issuer is not directly engaged by the sender to send an electronic transfer of funds to the foreign merchant; and

- A consumer’s deposit of funds into an account, including a for-benefit-of account, located in a state, because there has not been a transfer of funds to a designated recipient.

DISCLOSURES FOR REMITTANCE TRANSFERS

Pay From Away will provide a disclosure to a consumer before the consumer pays for a remittance transfer. The disclosure must be in writing, including electronically where permitted. The disclosure may also be given orally in telephone transactions where permitted.

The pre-payment disclosure must list:

- The exchange rate;

- Fees and taxes collected by Pay From Away, using the terms “transfer fees” and “transfer taxes”;

- Third-party fees charged by agents abroad and intermediary institutions, labeled as “other fees”;

- The amount of money expected to be delivered abroad, not including certain fees charged to the recipient or foreign taxes, labeled as “total to recipient”; and

- If appropriate, a disclaimer that other non-covered third-party fees and foreign taxes may apply.

Examples of covered third-party fees include:

- Fees imposed on a remittance transfer by intermediary institutions in connection with a wire transfer; and

- Fees imposed on a remittance transfer by an agent of the provider at pick-up for receiving the transfer.

The term non-covered third-party fees means any fees imposed by the designated recipient’s institution for receiving a remittance transfer into an account, unless the recipient institution acts as an agent of Pay From Away.

Pay From Away must also provide a receipt or proof of payment containing the required disclosures. The receipt must also inform consumers of the date on which funds will be available. Pay From Away will provide the disclosure in English. Where a sender transacts or asserts an error in another language, Pay From Away will use reasonable efforts to communicate in that language where feasible.

Under certain circumstances, Pay From Away may provide estimates. For example, when a sender schedules a one-time transfer, or the first transfer in a series of preauthorized remittance transfers, five or more business days before the date of transfer, Pay From Away may estimate certain information in the pre-payment disclosure and the receipt provided when payment is made. If disclosures with estimates are provided under this exception, Pay From Away will also provide the sender with an additional receipt containing accurate figures, generally no later than one business day after the date on which the transfer is made.

For preauthorized transfers, Pay From Away need not send a disclosure for each subsequent transfer, but will send a receipt within a reasonable time before the transfer if any information has changed from what was originally disclosed. This receipt may also contain estimates.

If estimates are provided or no update is necessary, Pay From Away may send an accurate receipt after the transfer is made.

Pay From Away must disclose the date of transfer in the receipt provided when payment is made with respect to remittance transfers scheduled at least three business days before the date of transfer and for the initial transfer in a series of preauthorized transfers.

Pay From Away must also disclose a transfer date on any subsequent receipts provided with respect to that transfer and any subsequent preauthorized transfers so that the sender can identify the transfer to which the receipt pertains and, when received before the date of transfer, can generally calculate the date on which the right to cancel will expire.

For subsequent preauthorized remittance transfers for which the date of transfer is four or fewer business days after payment is made for the transfer, Pay From Away will disclose future dates in the receipt provided for the first transfer in the series.

Pay From Away may describe on a receipt both the three-business-day and 30-minute cancellation periods and may either describe the transfers to which each deadline applies or use a checkbox or other method to designate which cancellation period applies to the transfer.

Appendix A of Regulation E (12 C.F.R. Part 1005) contains model forms that Pay From Away may use for pre-payment disclosures, error resolution disclosures, and cancellation disclosures.

SENDER’S RIGHT OF CANCELLATION AND REFUND

This policy directs management to implement procedures to ensure that Pay From Away responds in accordance with the requirements of 12 C.F.R. § 1005.34 with respect to any oral or written request to cancel a remittance transfer made by the sender no later than 30 minutes after the sender makes payment in connection with the remittance transfer, provided that:

- The request to cancel enables Pay From Away to identify the sender’s name and address or telephone number and the particular transfer to be cancelled; and

- The transferred funds have not been picked up by the designated recipient or deposited into an account of the designated recipient.

Pay From Away will refund, at no additional cost to the sender, the total amount of funds provided by the sender in connection with a remittance transfer, including any fees and, to the extent not prohibited by law, taxes imposed in connection with the remittance transfer, within three business days of receiving the sender’s request to cancel the remittance transfer.

ERROR RESOLUTION PROCEDURES FOR REMITTANCE TRANSFERS

Other than transactions subject to Regulation Z (12 C.F.R. Part 1026), Pay From Away will implement procedures to respond to notices of unauthorized remittance transfers. In accordance with 12 C.F.R. § 1005.33, this policy directs management to develop and maintain written policies and procedures designed to ensure compliance with the error resolution requirements applicable to remittance transfers.

Definition of an Error

An error includes:

- An incorrect amount paid by a sender in connection with a remittance transfer;

- A computational or bookkeeping error made by the remittance transfer provider relating to a remittance transfer;

- The failure to make available to a designated recipient the amount of currency stated in the disclosure provided for the remittance transfer, unless:

- The disclosure stated an estimate of the amount to be received and the difference results from the application of the actual exchange rate, fees, and taxes rather than estimated amounts; or

- The failure resulted from extraordinary circumstances outside the remittance transfer provider’s control that could not reasonably have been anticipated;

- The failure to make funds available to a designated recipient by the date of availability stated in the disclosure for the remittance transfer, unless the failure resulted from:

- Extraordinary circumstances outside the remittance transfer provider’s control that could not reasonably have been anticipated;

- Delays related to fraud screening procedures or compliance with the Bank Secrecy Act, Office of Foreign Assets Control requirements, or similar laws or requirements; or

- The remittance transfer being made with fraudulent intent by the sender or any person acting in concert with the sender; and

- The sender’s request for documentation or for additional information or clarification concerning a remittance transfer, including a request made by a sender to determine whether an error exists.

The term error does not include:

- An inquiry about the status of a remittance transfer, except where the funds were not made available to a designated recipient by the disclosed date of availability;

- A request for information for tax or other recordkeeping purposes;

- A change requested by the designated recipient; or

- A change in the amount or type of currency received by the designated recipient from the amount or type of currency stated in the disclosure, if Pay From Away relied on information provided by the sender in making such disclosure.

TIMING AND CONTENT REQUIREMENTS

Pay From Away will comply with the error resolution procedures in Subpart B of Regulation E when it receives an oral or written notice of error no later than 180 days after the disclosed date of availability of the remittance transfer, and Pay From Away is able to identify the following information:

- The sender’s name and telephone number or address;

- The recipient’s name and, if known, the telephone number or address of the recipient;

- The remittance transfer to which the notice of error applies; and

- The reason the sender believes an error exists, including to the extent possible the type, date, and amount of the error, except for requests for documentation and additional information.

Requests for Documentation or Clarification

When a notice of error is based on documentation, additional information, or clarification previously requested by the sender, the notice is timely if Pay From Away receives it on the later of:

- 180 days after the disclosed date of availability of the remittance transfer; or

- 60 days after Pay From Away sent the documentation, information, or clarification that had been requested.

Time Limits and Extent of Investigation

Pay From Away will promptly conduct an investigation to determine whether an error occurred within 90 days of receiving a notice of error. Pay From Away will report the results to the sender, including notice of any remedies available for correcting any error, within three business days after completing the investigation.

If Pay From Away determines that an error occurred, it will correct the error as designated by the sender within one business day of, or as soon as reasonably practicable after, receiving the sender’s instructions regarding the appropriate remedy. As appropriate, Pay From Away will either:

- Refund the amount of funds provided by the sender in connection with a remittance transfer that was not properly transmitted, or the amount appropriate to resolve the error; or

- Send the original amount as requested by the sender.

If the error resulted because the recipient did not receive the amount by the date initially disclosed, then Pay From Away will do one of the following, as applicable:

- Refund to the sender the amount of funds that was not properly transmitted, or the amount appropriate to resolve the error;

- Make available to the designated recipient the amount appropriate to resolve the error, without additional cost to either party; or

- Refund any fees to the sender and, to the extent not prohibited by law, taxes imposed for the remittance transfer, unless the sender provided incorrect or insufficient information to Pay From Away in connection with the remittance transfer.

In the case of a request for additional information, Pay From Away will provide the requested documentation, information, or clarification.

Procedures if Pay From Away Determines No Error or a Different Error Occurred

If Pay From Away determines that no error occurred, or that a different error occurred, Pay From Away will:

- Send a written explanation of its findings and note the sender’s right to request the documentation on which Pay From Away relied in making its determination. The explanation will also address the sender’s specific complaint; and

- Promptly provide copies of the documents on which Pay From Away relied in making its error determination.

If Pay From Away has fully complied with the requirements of 12 C.F.R. § 1005.33 and the sender still believes an error occurred, Pay From Away will have no further responsibilities under the regulation.

Appendix A of Regulation E (12 C.F.R. Part 1005) contains model forms that management may use to provide Pay From Away with a safe harbor for the content of pre-payment disclosures, error resolution disclosures, and cancellation disclosures.

REVIEW

Management will review this policy at least annually and make any changes deemed necessary to comply with revisions to the regulations implementing the Electronic Fund Transfer Act, or whenever management determines that the policy should otherwise be strengthened or broadened.

RECORD RETENTION

Records showing compliance with applicable EFTA requirements will be retained for a period of not less than two years from the date disclosures are required to be made or action is required to be taken.

APPENDIX A

Procedures EFTA Reg E - ERROR RESOLUTION FLOW CHART

Applies to Consumer Accounts Only

IMPORTANT: Refer to clarifying details and consumer liability calculations on next page.

EFTA Reg E - ERROR RESOLUTION QUICK REFERENCE GUIDE

Regulation E Section 205.11 defines seven types of EFT errors that qualify for the resolution process noted on the previous page.

- An unauthorized transaction is a transaction that was initiated by someone other than the account holder and the account holder did not receive any benefit from the transfer. An unauthorized transaction does not include:

- An EFT made with fraudulent intent by the consumer or a person acting in concert with the consumer;

- An EFT error committed by a financial institution or its employees; or

- An EFT initiated by a person other than the consumer owner to whom the consumer owner furnished the card, code, or other means of access, unless the owner notified the institution that transfers by that other person are no longer authorized.

- Incorrect EFT to or from the consumer account.

- Omission of an EFT from a statement or transaction record.

- An EFT computational or bookkeeping error made by the financial institution or provider.

- Receipt of an incorrect amount of money at an ATM or other cash-dispensing terminal.

- EFT not properly identified and the consumer does not recognize the transaction.

- Consumer request for clarification or other information or documentation to determine whether an error was made.

Error Resolution Responsibilities

- The consumer must notify the institution or provider as soon as an error is known or suspected.

- The institution or provider must investigate and quickly resolve the potential error within the appropriate time period.

Consumer Responsibilities

- To limit the consumer’s liability, oral or written notice must be provided:

- Within 2 business days following learning of the loss or theft of an access device; or

- Within 60 calendar days of transmittal of the statement containing the first error if no access device was lost or stolen.

- It is the institution’s option to require written notice within 10 business days of verbal notice in order for the consumer to receive provisional credit. The written notice should include the consumer’s name, account number, and description of the error. If written notice is not provided within 10 business days, the consumer is not entitled to provisional credit, but the investigation must still be completed on a timely basis within the applicable 45- or 90-day period.

Consumer Negligence

- Negligence on a consumer’s part cannot be considered to impose more liability on the consumer than allowed under Regulation E.

- If the consumer writes a PIN on a card or on paper attached to the card, the institution cannot claim consumer negligence and impose additional burden on the consumer. Card network rules may differ for chargeback processing in cases involving consumer negligence.

Consumer Liability Calculations

Select the appropriate chart based on whether the consumer’s access device was lost or stolen, such as a debit card or online banking credentials, or whether the transaction was first noted on the account statement or transaction record, such as an unauthorized ACH transaction, incorrect amount, or counterfeit debit card transaction.